How to Build Wealth In Your 40s

It’s never too late to improve your financial situation. Learn how to build wealth in your 40’s with strategies for retirement, homeownership, and more.

Building wealth in your 40s involves making a plan and taking concrete steps towards reaching your goals. The median net worth is $91,300 for ages 35-44, and $168,600 for ages 45-54. Retirement should be a priority in your finances. The average retirement age in America is 62, which means you have just a few decades to get your finances in order. The key to building real wealth is to make your money work for you while you’re sleeping. This can be achieved by investing, using high-yield savings products like Tellus, or by investing in income-producing assets.

If you’re approaching middle age, you may be concerned about building wealth for your future. This guide will cover how to build wealth in your 40s to help you achieve financial freedom and security.

In your 40s, retirement savings should often be a primary focus — but retirement is far from the only savings goal you should be pursuing. Wealth is a broad term that encapsulates retirement savings, real estate, and other assets that can help you build financial security.

Below, find out everything you need to know about building wealth in your 40s — starting with how you might compare to peers in your age group.

Contents

Average net worth in your 40s

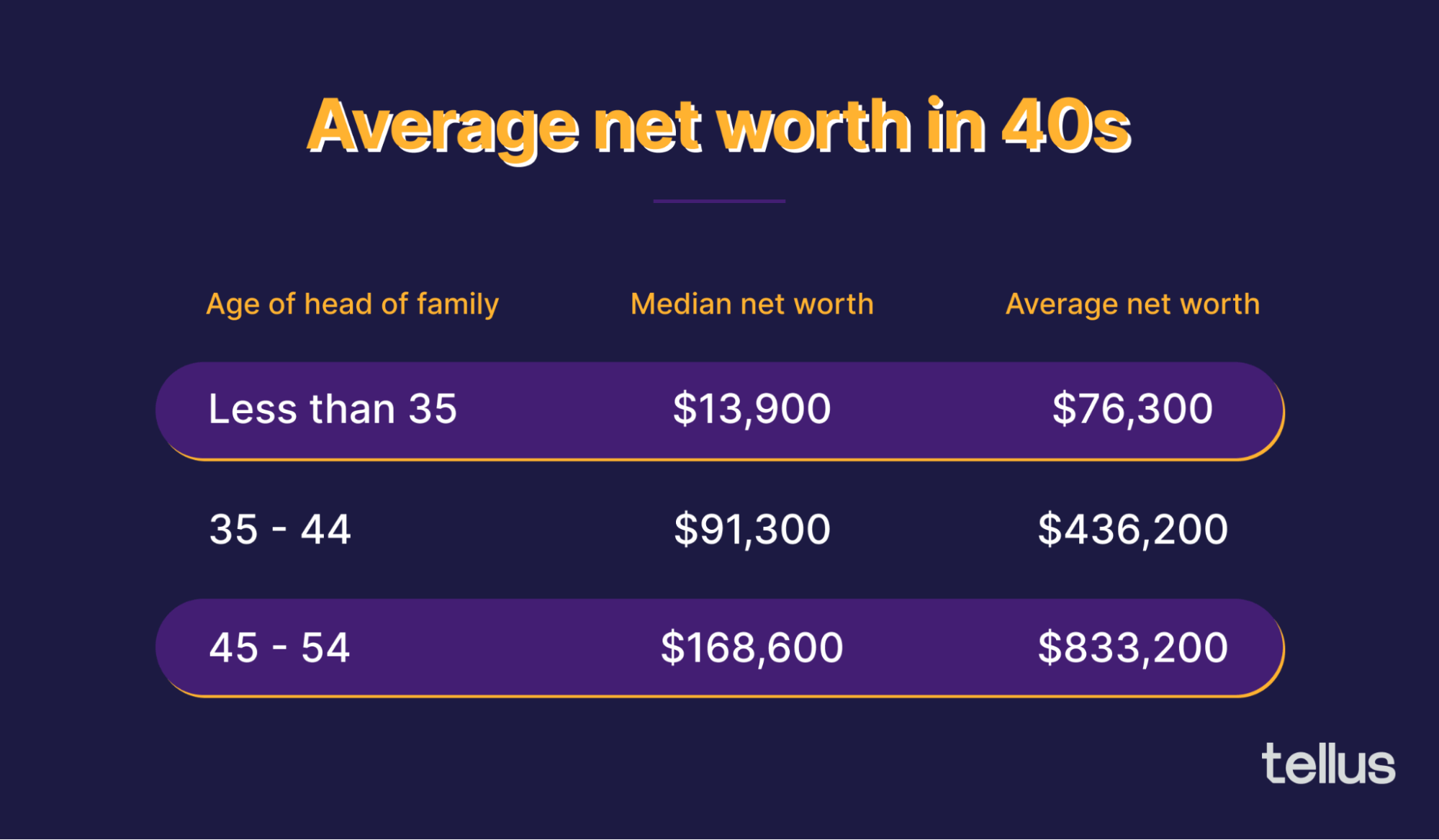

Everyone is on their own journey to building wealth. With that said, it can be helpful to check in with how your progress stacks up against your peers in a similar age group. The image below outlines average net worth by age, based on data from a 2019 Federal Reserve survey.

Based on this data, we can see that the average net worth for ages 34-44 is $436,200, while the average for ages 45-54 is $833,200.

These are averages, which are often skewed by very high-wealth households. For example, there are billionaires in that age category that drastically skew the results.

A more accurate representation is using the median net worth. This is the center point in the set of data points and is often a more accurate way to measure the net worth of a typical family. This way of measuring gives less weight to extreme outliers, like multi-millionaires.

The median net worth is $91,300 for ages 35-44, and $168,600 for ages 45-54.

How to build wealth in your 40s

Building wealth in your 40s is like any other time in your life — it involves making a plan, taking concrete steps towards reaching your goals, and staying consistent.

Regardless of your life situation, there are some principles of wealth building that you can utilize to reach your goals. Here’s what to consider.

Prioritize retirement savings

In your 40’s, retirement should absolutely be a priority in your finances. The average retirement age in America is 62, which means you have just a few decades to get your finances in order.

And most people will need substantial savings to enjoy a comfortable retirement. Experts recommend that you be able to access between 70% and 90% of your pre-retirement income once you retire. So if you earn $100,000, you should aim to have $70,000 to $90,000 in income during retirement.

Using the 4% rule, which states that you can safely withdraw 4% of your retirement savings each year, this would mean that you would need between $1,750,000 and $2,250,000 in savings.

This calculation ignores the impact of social security and other benefits — but nonetheless, it illustrates that most people will need substantial savings in order to retire.

In most cases, you should aim to contribute as much as possible to retirement accounts, such as a 401(k) or Roth IRA. This is particularly true if your employer offers 401(k) matching — more on this below.

Maximize employer benefits

Many employers offer benefits that can help you build wealth. 401(k) matching is a major perk offered by around 98% of 401(k) plans. Matching means that the employer will match a certain percentage of the funds you contribute to your retirement account.

For example, a company might offer 100% matching up to 6% of salary. If you earn $100,000, your employer would match the first $6,000 in contributions you make to your 401(k) each year.

If your employer offers this perk, make sure to take advantage of it.

Other workplace perks should also be optimized for wealth-building. Your employer may offer health insurance, a health savings account (HSA), and other lucrative benefits. Be sure to check with your workplace's Human Resources department for details on all your benefits.

Reduce high-interest debt

Debt can be a drag on your finances, particularly if it’s high-interest debt like credit cards or personal loans. If you have high-interest debt, paying it off should be a top financial priority.

It may be wise to prioritize credit card debt over investing. The average credit card APR is over 15%, while the stock market tends to return around 10% per year, on average. Put simply, this means you could theoretically expect to earn 10% per year by investing, but you could save 15% per year by paying off credit card debt.

Plus, once you pay off debt, you’ll have more room in your budget to save toward your financial goals. In other words, you can pay off debt first, then play catch-up on your investments using the amount you’d typically spend on debt repayments.

Avoid lifestyle creep

“Lifestyle creep” is the concept of gradually spending more money as you earn more money. You get a raise at work, so you move to a bigger condo. Or you start up a side-hustle and reward yourself with an extra meal out every week.

While some level of increased costs is to be expected, it’s important to keep these urges in check. Otherwise, spending just about all the money you earn can become very easy. In fact, around 30% of those earning $250,000 or more still live paycheck-to-paycheck.

To avoid lifestyle creep, it’s helpful to appreciate what you have and keep an eye on your monthly budget. How much are you spending on each category, and does your spending align with your values and goals?

It’s also helpful to realize that relatively small changes in your spending habits can produce huge results over the years. Investing an extra $200 per month would boost your retirement savings by over $100,000 over a 20-year period (assuming 7% average stock market returns).

Expand income streams

You’ll be better set up for wealth building if you can earn income from multiple sources. Diversifying income can also help protect you from economic shocks, like the loss of a job.

There are many ways to expand your income streams. You could consider:

- Purchasing a rental property

- Starting a side hustle

- Starting or buying a small business

- Renting out part of your home

- Getting a second job

The idea is simply to diversify your income. Passive income streams can be particularly powerful, as they won’t require much (or any) of your active time.

Plus, because you’re already used to living on your primary income, you can likely save 100% of the income from this new source.

For example, if you pick up a side hustle that earns you an extra $300 per month, invest that $300 per month in your retirement fund. In 20 years, you’ll have over $150,000 extra in your account (assuming 7% average returns).

Tellus, a cash rewards app is also a great option. Tellus turns your money into passive income. Learn more here.

Downsize your home

It’s also worthwhile to take a look at your current home and determine whether or not it exceeds your needs. Perhaps you have children that have since moved out, and you have several spare bedrooms. Or maybe you’re just living in a home with space that you simply don’t utilize much.

Downsizing to a smaller living space can drastically reduce your expenses. Your rent or mortgage payments will be lower, as will your utilities and property taxes.

Make your money work for you

The key to building real wealth is to make your money work for you while you’re sleeping.

This means that your savings should be earning you money. This can be achieved by investing, using high-yield savings products, or by investing in income-producing rental properties.

There are a few different approaches here, depending on your goals and tolerance for risk.

Investing in stocks

Buying stocks or stock market index funds is a powerful way to build long-term wealth. On average, the S&P 500 has returned around 10% per year. At that rate, $1 invested today will grow into over $17 after 30 years.

However, stocks carry risk. Returns are inconsistent, and sometimes markets decline significantly. For this reason, investing in stocks is typically best reserved for long-term financial goals, such as retirement.

It’s riskier to invest short-term and medium-term savings. For instance, if you have a down payment saved up that you plan to use in the next several years, it’s riskier to invest in stocks. Nobody can predict the short-term movements of the stock market.

Real estate investing

Buying real estate to rent out is another way to make your money work for you. This provides exposure to growth in the real estate market, as well as a monthly source of income from rents.

The profitability of real estate investing varies based on location and other factors. In some markets, it’s a great opportunity — in others, investing in the stock market may be a better option. This beginner's guide to real estate investing should get you started.

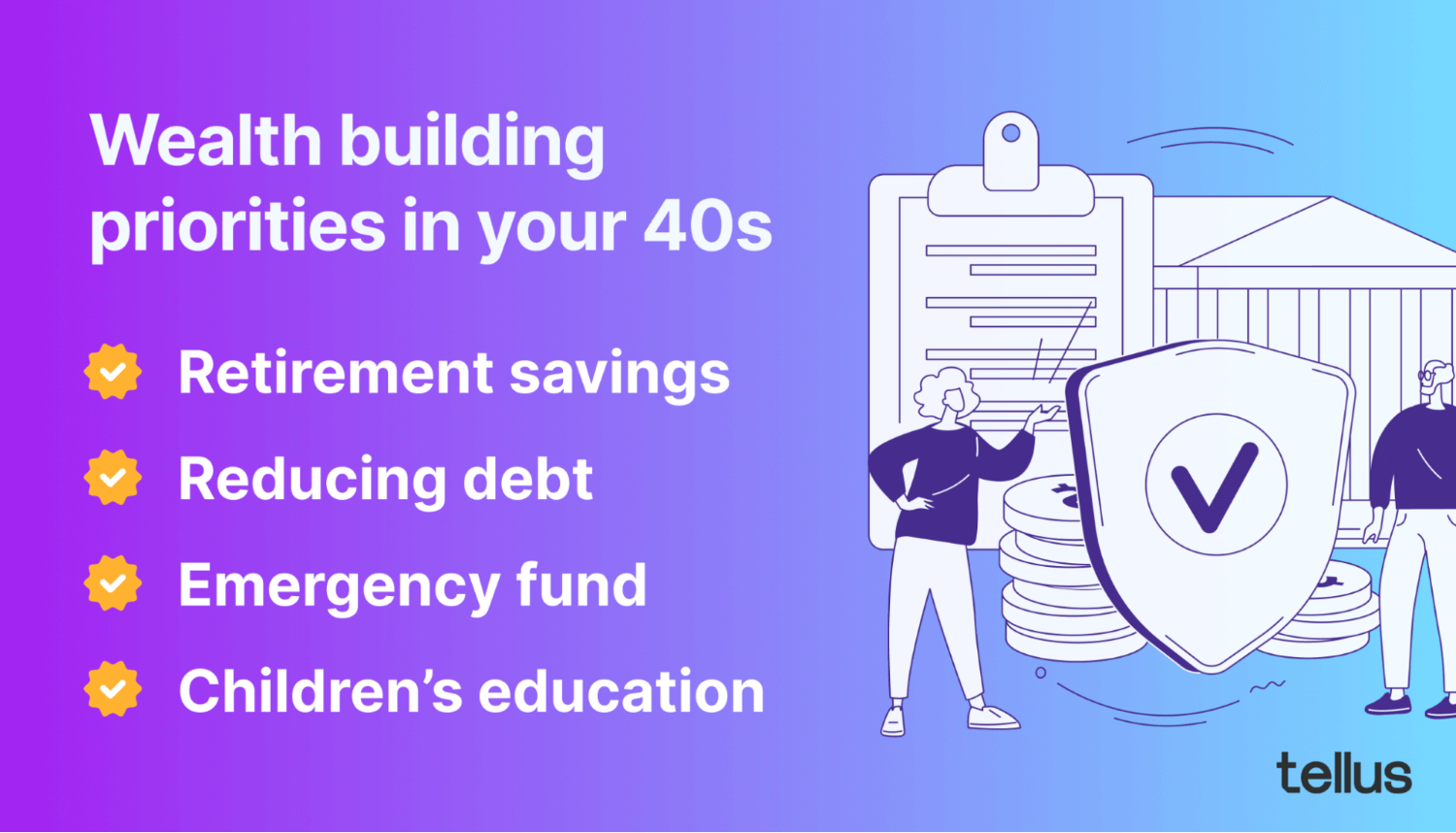

Wealth-building priorities in your 40s

“Wealth” is typically defined as your net worth, which is all your assets minus all your debts.

Anything that increases your net worth increases your wealth — but that doesn’t mean you shouldn’t prioritize certain goals. Here are four wealth-building priorities for your 40s.

Retirement savings

Retirement should be a top priority. Fidelity recommends that you have at least 3x your income invested by age 40 and at least 6x your income by age 50. So if you earn $75,000 per year, you should aim to have $225,000 invested in retirement funds by age 40 and $450,000 by age 50. If you’re working toward early retirement, you’ll need even more saved by these benchmark ages.

It’s important to maximize contributions to retirement accounts because of the generous tax perks they offer. Retirement funds should almost always be kept in tax-advantaged retirement accounts, such as a 401(k) or Roth IRA.

Traditional retirement accounts offer an upfront tax break. If you contribute $5,000, you can deduct that from your current year's taxable income. Plus, your money can grow tax-deferred until retirement.

Roth retirement accounts offer no upfront tax break, but you won’t have to pay income tax when you eventually withdraw funds in retirement.

Plus, many employers offer matching perks on 401(k) accounts. This means that your employer will kick in some extra funds if you make contributions to your 401(k).

Reducing debt

Debt creates a significant drag on your expenses and your net worth. Doing whatever you can to reduce your debt can save you money on interest and free up more money in your monthly budget.

The higher the interest rate, the more aggressively you should aim to pay off the debt. Credit cards, personal loans, and other high-interest debt should be the first to go. If you have credit card debt, paying it off may even take priority over investing.

On the other hand, mortgages and most car loans are relatively low-interest. These can be a lower priority — but should still be on your radar.

Emergency fund

An emergency fund is a chunk of money set aside for unexpected expenses and/or unexpected loss of income. It’s very important for financial security.

Most experts recommend that you have 3 to 6 months of expenses saved in an emergency fund. If your household spends $5,000 per month, that’s $15,000 to $30,000 for an adequate emergency fund.

This money should be kept in liquid savings that can be accessed at any time. It’s best not to invest these funds, as you may be forced to sell at a loss if the stock market declines.

Children’s education

If you have children, saving for their education should also be on your financial to-do list. The average cost of college is now $35,331 per student per year, and this cost is growing at a rate of over 6% per year.

While many students may qualify for financial aid or scholarships, most students will have out-of-pocket expenses.

Parents can save for their children’s future using a college savings account. A 529 plan is a good option, as it provides tax benefits.

529 plans allow parents to contribute funds, which can then be invested. Funds can grow tax-deferred. When funds are eventually withdrawn, they can be accessed tax-free, as long as they are used for qualifying educational expenses.

The downside is that there are tax penalties if funds are used for anything other than educational expenses. It’s best only to use a 529 if you are confident that your children will attend college.

Wrapping up

Ultimately, building wealth in your 40s involves working toward your various financial goals over the long term. From a comfortable retirement to owning your own home, the real key is consistency.

Financial priorities for those in their 40s include saving for retirement, building an emergency fund, reducing debt, and saving for major expenses like a child’s college education. By planning ahead, you can balance all these various priorities and make consistent progress towards all your goals.

{kind=link}