How to Build Wealth In Your 30s

In your 30s, your finances can really kick off. Here’s how to maximize your earnings, investments, and more to start building real wealth in your 30s.

The amount of money you can save in your 30s will depend on your income, outgoings, saving priorities, and future plans. There are several ways to build wealth in your 30s, including maximizing employer benefits, reducing debt, managing spending, and putting your money to work Lifestyle and future plans can impact priorities. But everyone should prioritize reducing debt and saving for retirement. Other considerations include purchasing a home and saving for your children’s future.

Money won’t buy happiness, but it can certainly buy a lot of peace of mind! If you want a stable financial future, it’s all about taking consistent steps to build wealth. And the earlier you can get started, the better.

Your 30s are a great time to build wealth. By this point, you likely have a stable income and may be part of a dual-income household. This can be a powerful foundation for wealth building.

There’s no single path to wealth, but rather a combination of helpful steps you can take. Here’s how to build wealth in your 30s.

Contents

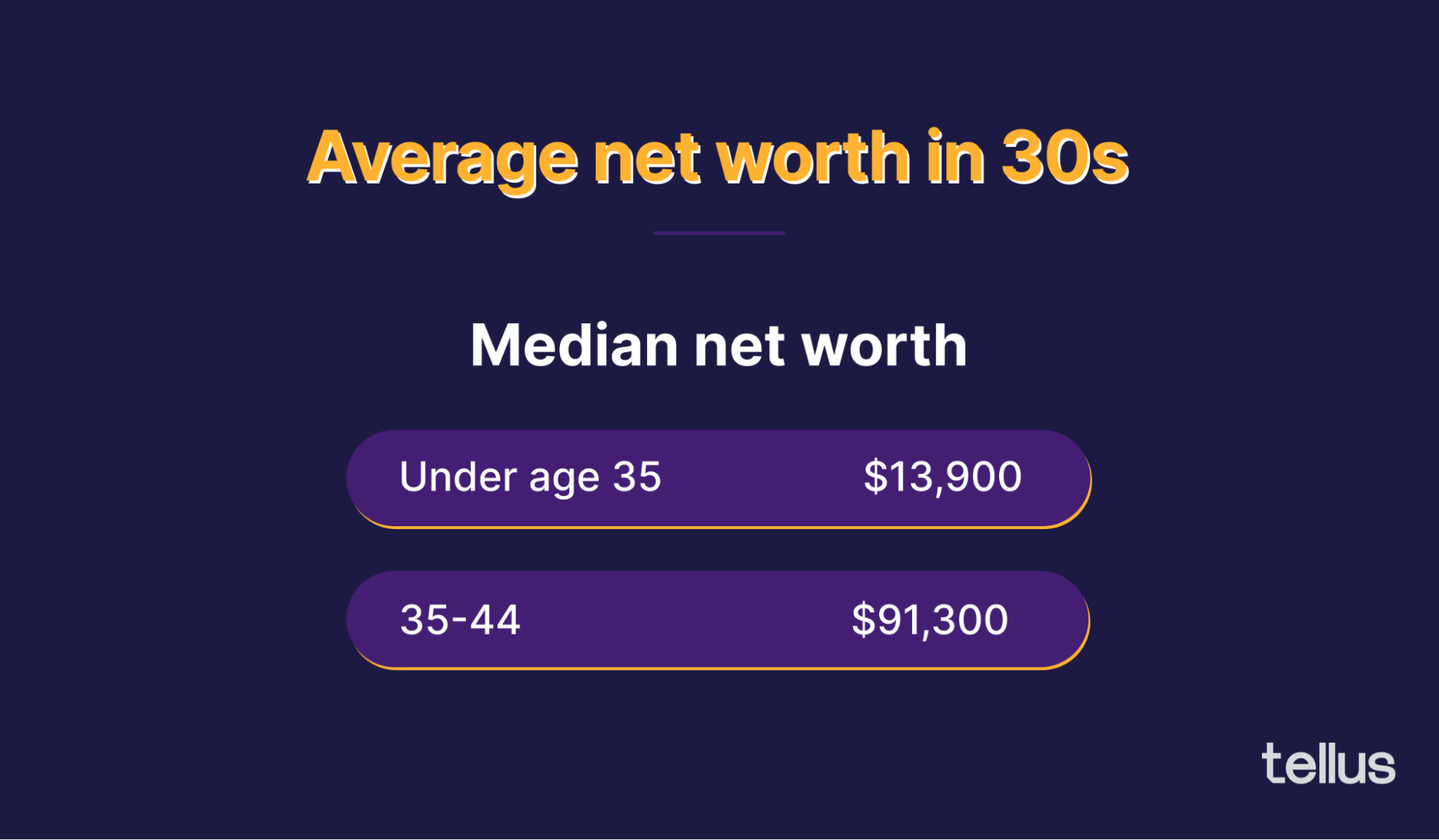

Average net worth by age 30

Wealth is typically measured by net worth, calculated by total assets minus total debts. For example, if you have $5,000 in savings, $25,000 in retirement accounts, and $3,000 in credit card debt, your net worth is $27,000.

Curious how you stack up with your peers? Read through our guide on how much you should have saved by age 30, then take a look at the median net worth data for Americans in their 30s.

According to a 2019 Federal Reserve study (the latest available data), the median net worth for those under age 35 was $13,900. For those 35-44, the median net worth was $91,300.

Average net worths typically trend higher for older age groups. Those in their low thirties tend to have fewer assets than those in their mid-to-late thirties.

The true “average” net worth is higher than these figures, but averages are skewed higher by extremely wealthy households. The more accurate measure is the median, which represents the midpoint in a set of data.

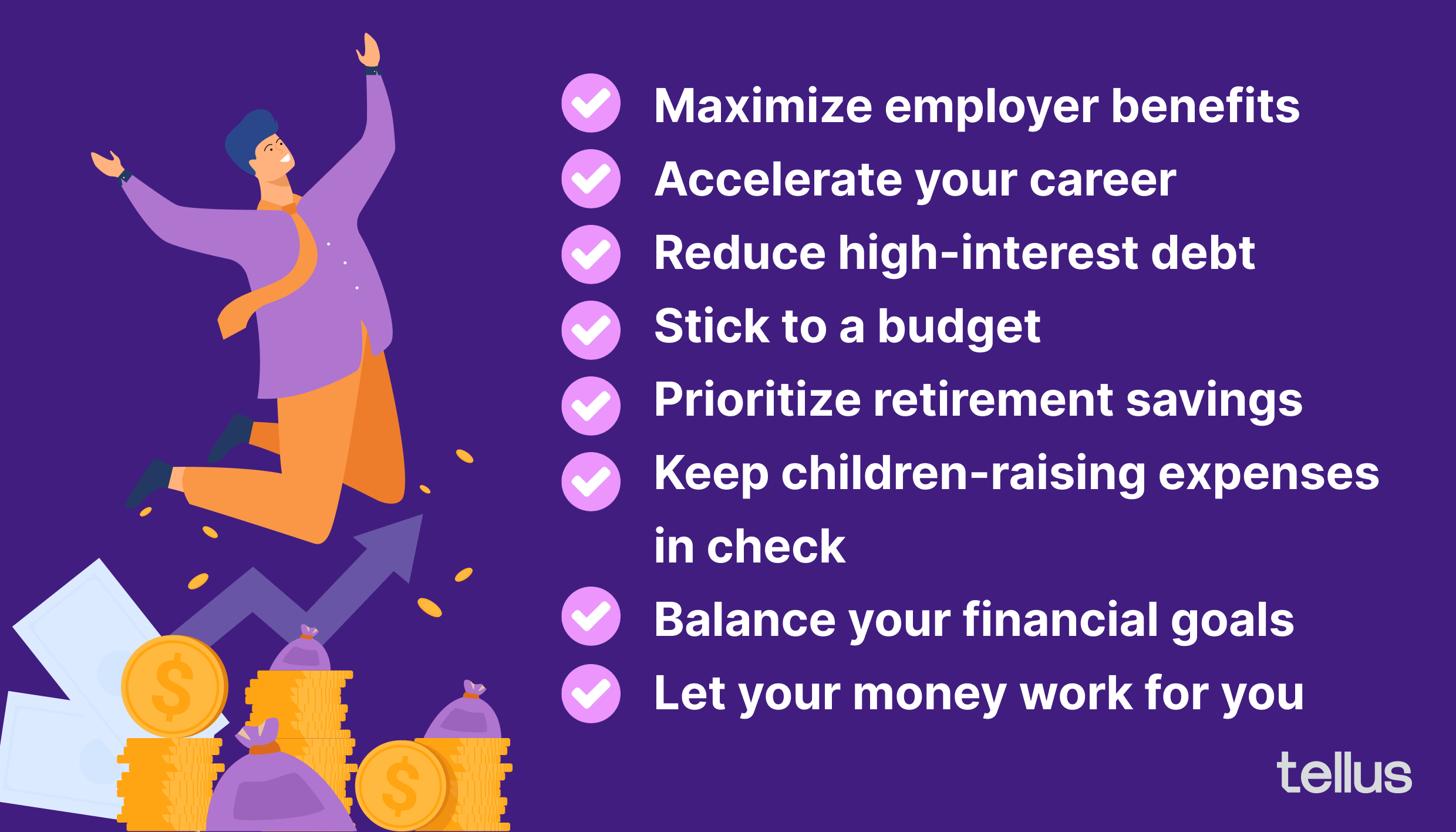

How to build wealth in your 30s

Your 30s can be a good time to build wealth and set up a financial foundation for your future. It’s a good time to pursue career advancements, take advantage of employer benefits, and begin investing for the future.

Your 30s are also a time to start evaluating your spending habits and make shifts to align your spending with your goals.

Here are some important factors for building wealth in your 30s:

Maximize employer benefits

It’s wise to take full advantage of any benefits offered by your employer.

Employer benefits vary, but some of the most valuable include:

- Health insurance benefits (which may even cover family members)

- Retirement benefits and pensions

- Paid time off

- Paid medical leave

- Paid training

- And more

Some employers will even pay for ongoing education, particularly if that education helps advance your career. Others may offer side perks like a free gym membership, mental health counseling, or life insurance.

Always make sure you’re enrolled in any optional benefits programs and follow up with the human resources department if you have any questions.

Accelerate your career

In your 30s, you’re likely in a great position to accelerate your career and, therefore, your earnings.

This could mean working hard at your current position to pursue a promotion or looking around for other job opportunities (even when you have a stable job).

In any case, investing in yourself and your career is wise. That could mean going back to school to get another degree or certificate, or it could simply mean attending networking events in your industry.

Reduce high-interest debt

Debt can be a huge drag on your wealth-building progress. This is particularly true of high-interest debt, like credit cards and personal loans.

Credit cards have average interest rates of over 20%, making them a very costly form of debt. Rates on personal loans and payday loans can be even higher.

Paying down these debts is a win-win. It directly increases your net worth by lowering your debt load and your monthly expenses by reducing monthly debt payments.

In some cases, it might even make sense to prioritize debt payments over investing. Investing is a great way to build wealth — the US stock market has returned over 10% per year, on average, since the 1950s. But if you’re paying 20% interest on credit card debt, you may be better off paying this debt down first before pursuing investments.

Stick to a budget

Most households will see their income levels increase during their 30s. This is welcome news — but when you earn more, it’s easier to spend more as well. This is often referred to as “lifestyle creep.” As your income rises, it becomes easier to justify increased spending on optional items.

If your priority is building wealth, it pays to keep spending in check. The best way to do this is to build a budget — and stick to using it!

It may also be helpful to use a budgeting app, like Mint or YNAB, to track your spending and monitor your progress.

Prioritize retirement savings

Saving for retirement should be a priority throughout your life. And the earlier you get started, the better. Because of compounding interest, investments you make early in life have more time to grow. The effects of early investments can be quite significant.

On the other hand, if you wait to start investing, you’ll have to save much more to reach your goals.

To illustrate this, consider this example:

- Your goal is to have $1,000,000 saved by age 65

- You assume 10% average returns in the stock market

- If you start at age 30, you need to save only $307.47 per month to reach your goal

- If you start at age 40, you need to save $847.33 per month to reach your goal

By waiting 10 years to start investing, you would have to save nearly 3x as much per month to reach the same target savings goal.

Curious to plan out your savings goals? Use this savings goal calculator from Investor.gov.

Keep children-raising expenses in check

If you have or plan to have children, prepare for a significant increase in costs. Recent estimates show that in the US, it costs over $310,000 to raise a child to age 17. That’s over $18,000 per year, or $1,500 per month — although costs aren’t necessarily spread out so evenly.

It’s important to be realistic about the increased costs you can expect while also taking steps to keep expenses in check. This could mean:

- Buying used clothing, toys, bikes, etc.

- Utilizing hand-me-downs from family and friends

- Buying food in bulk

- Utilizing family to help with childcare

It’s a good idea to adjust your budget for the upcoming increase in expenses while working to build up a savings fund set aside for unexpected expenses.

Balance your financial goals

Financial progress is all about finding balance. In your 30s, you’re likely juggling a lot of different financial plans and priorities — and taking active steps to find a balance is important.

To do this, it’s helpful to sit down and put your plans on paper. Identify your goals, and list them all on paper.

Then, figure out how much money you have available to spend or save every month, and decide how much to allocate to each specific goal.

For instance, you might have $700 that you can set aside every month. From that, you may decide to put $300 toward retirement, $100 toward your child’s future education, $200 towards debt payments, and $100 toward a general savings account.

Wealth-building priorities in your 30s

There are many financial responsibilities and goals to juggle as a 30-something. What should you prioritize?

Reducing debt

Debt creates a direct drag on your financial progress. Getting out of debt should be a priority for most households.

However, not all debts are created equal.

High-interest debts, like credit cards, payday loans, and personal loans, should be paid off as quickly as possible. The sky-high interest rates on these forms of debt can create a huge drag on your financial progress.

Lower-interest debts, like mortgages, are less of a priority. You will, of course, need to make the required monthly payments on all your debts, but making extra payments toward a mortgage loan often doesn’t make financial sense. Often, it makes sense to invest extra money rather than make extra payments on low-interest debt.

Maximizing retirement savings and tax benefits

Saving for retirement is incredibly important, and early savings will have a much greater impact in the long run.

Saving in a dedicated retirement savings account (401(k), Roth IRA, etc.) can also provide you with generous tax benefits. Maximizing these benefits early on can give your savings a significant boost.

The IRS provides tax breaks to help encourage people to save for retirement. These tax benefits are only earned if you save in a dedicated retirement account.

Most workplaces offer 401(k) accounts, which offer upfront tax perks when you make a contribution.

For example, if you earn $60,000 per year, making a $1,000 contribution to a 401(k) could earn you a tax break of around $220. Making a $5,000 contribution could earn you a tax break of over $1,100!

For best results, it’s recommended to invest the money you save from these tax breaks when you get your refund each year.

Purchasing a home

Homeownership is a primary goal for many households. Owning your home can help you build wealth and potentially reduce your long-term housing costs.

However, purchasing a home is a major undertaking that requires careful planning.

The biggest hurdle is often saving up enough for a down payment.

At the very least, mortgage lenders require a down payment of 3% of the home’s value. On a $500,000 home, that’s $15,000. But many experts recommend saving much more — the “gold standard” is often considered 20% or $100,000 on a $500,000 home.

Buying a home also requires good credit and consistent income. Lenders consider your debt-to-income ratio, credit score, down payment amount, and other factors when considering you for a mortgage loan.

To prepare for buying a home, it’s important to make a detailed plan. This should include how you will save up for a down payment, improve your credit as much as possible, and pay for closing costs, moving expenses, and other one-time expenses associated with home buying.

Saving for your children’s education

If you have children, saving for their future should be on your radar. Many parents choose to save for their children’s college education, especially considering that the average total cost to attend college is now over $35,000 per year.

Parents saving for their children’s future education can utilize college savings accounts like a 529 plan. These accounts offer tax benefits if savings are used for qualifying education expenses, and funds within a 529 can typically be invested for long-term growth.

529 plans can be opened with brokerage companies (Fidelity, Vanguard, Schwab, etc.) as well as with certain banks. However, plan details vary by state, so be sure to research the specifics before opening an account.

Wrapping up

In your 30s, your income is likely increasing — but so are your expenses! It’s a tricky decade to optimize your finances, but wealth building is all about finding balance. Try to take small, consistent steps toward all your financial goals simultaneously. Remember, even small amounts saved consistently over time can have huge results!

{kind=link}