How much of my paycheck should I save?

This guide looks at expert advice and common savings strategies to answer this common question.

Most Americans are paid twice per month. And for many households, everyday expenses are eating up more and more of their paychecks.

Even so, it’s important to save money where you can. Whether you’re saving toward your retirement or shorter-term goals like a vacation, it’s always a good idea to set aside some money from each paycheck.

But how much of your paycheck should you save? This guide looks at expert advice and common savings strategies to answer this common question.

How much of my paycheck should I save?

One of the most common recommendations is that you should aim to save around 20% of your income.

This recommendation to save 20% is part of the 50/30/20 budget, a budget planning strategy we cover in more detail later. It’s also a common recommendation from many financial experts and authors.

While 20% is a great rule of thumb, it won’t fit everyone’s budget and earnings. And it won’t fit into everyone’s goals for their finances.

If you’re like the 78% of Americans living paycheck to paycheck, 20% can be almost impossible to reach. On the other hand, if you’re part of a high-income household and you want to retire early, you may wish to aim even higher than 20%.

Additionally, that 20% may be split between actual savings and debt repayments. If you have high-interest debt, making extra payments toward those debts makes more financial sense than depositing money in a savings account.

Lastly, consider that 20% of your income doesn’t necessarily mean 20% of every paycheck. You might choose to save 10-15% and save any bonuses, gifts, or tax refunds you get to make up the rest. Or, for couples, you may choose to save 20% of your combined income rather than 20% from each paycheck.

Here’s the simple answer: You should aim to save around 20% of your income if you can. If you can’t do that, aim to save as much as possible.

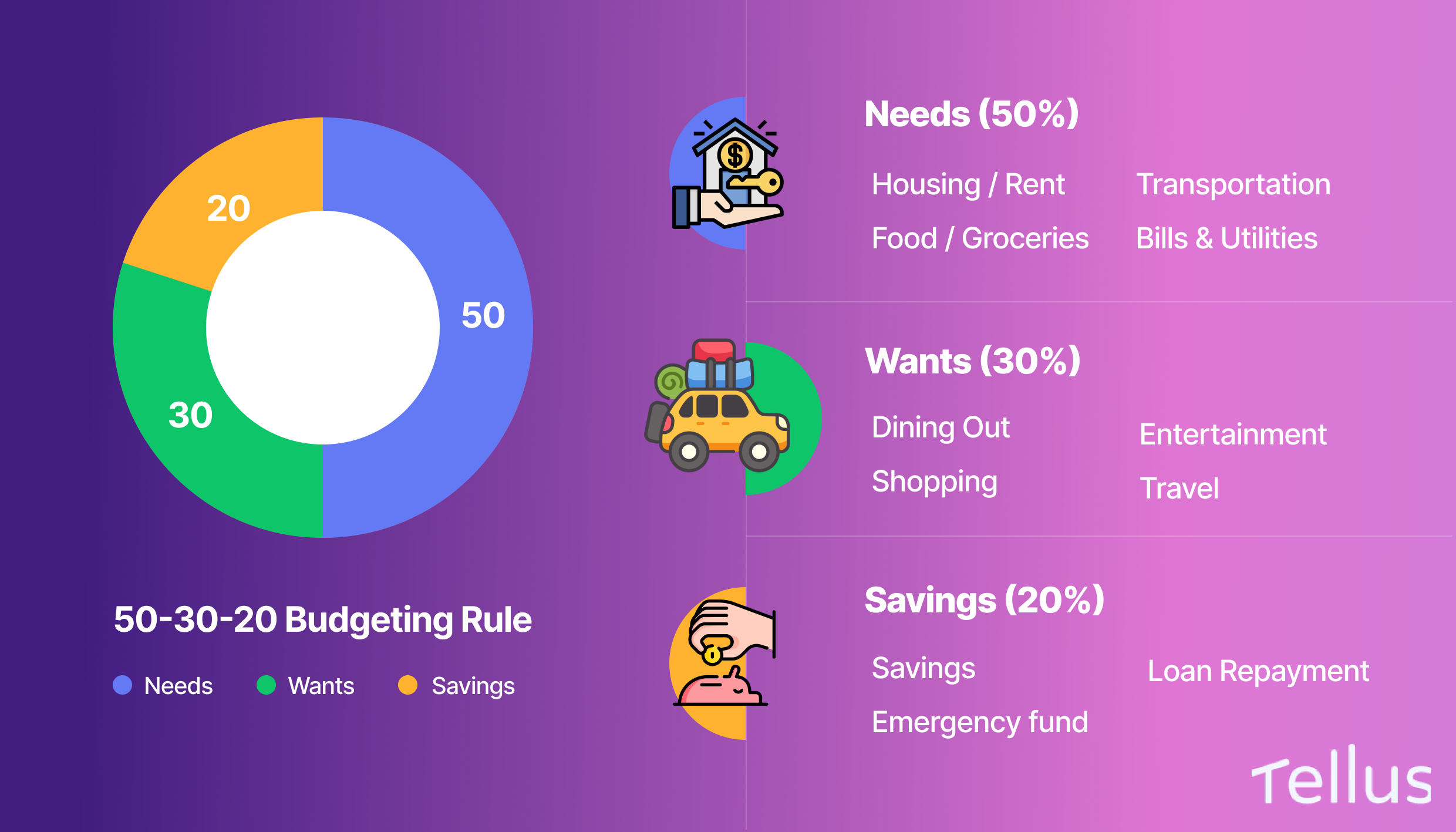

The 50/30/20 budgeting rule

How much of my paycheck should I save vs. spend? And how much of my budget should go toward wants vs. needs? The 50/30/20 budget rule answers all of these questions.

The 50/30/20 framework states that 50% of your budget should go toward needs, 30% toward wants, and 20% toward savings & debt repayment.

Needs refers to essential expenses like rent, transportation, groceries, and bills.

Wants refers to optional expenses, like entertainment, travel, and restaurants.

Savings refers to saving money toward various goals (retirement, buying a house or apartment, emergency fund, etc.) and repaying loans.

This framework is a useful starting point for building a budget. Let’s look at a few examples to illustrate.

A young working couple has a combined after-tax income of $8,000 per month. Following the 50/30/20 rule, they will have:

- $4,000 to spend on needs, like housing and groceries

- $2,400 to spend on wants, like dining out and travel

- $1,600 to save or use for debt repayments

A single parent has an after-tax income of $3,000 per month. Following the 50/30/20 rule, they have:

- $1,500 to spend on needs

- $900 to spend on wants

- $600 to save or use for debt repayments

As you can see from these two examples, the rule is more of a starting point than a firm guideline.

In the first example, the couple has $2,400 per month to spend on wants — which could easily be reduced to save more.

On the other hand, in the second example, the single parent only has $1,500 to spend on essentials — which may be too low. He may need to reduce his spending on wants and/or his savings in order to cover his basic expenses.

How much should I save towards each financial goal?

We know that saving around 20% of our income is good. But where should those savings actually go?

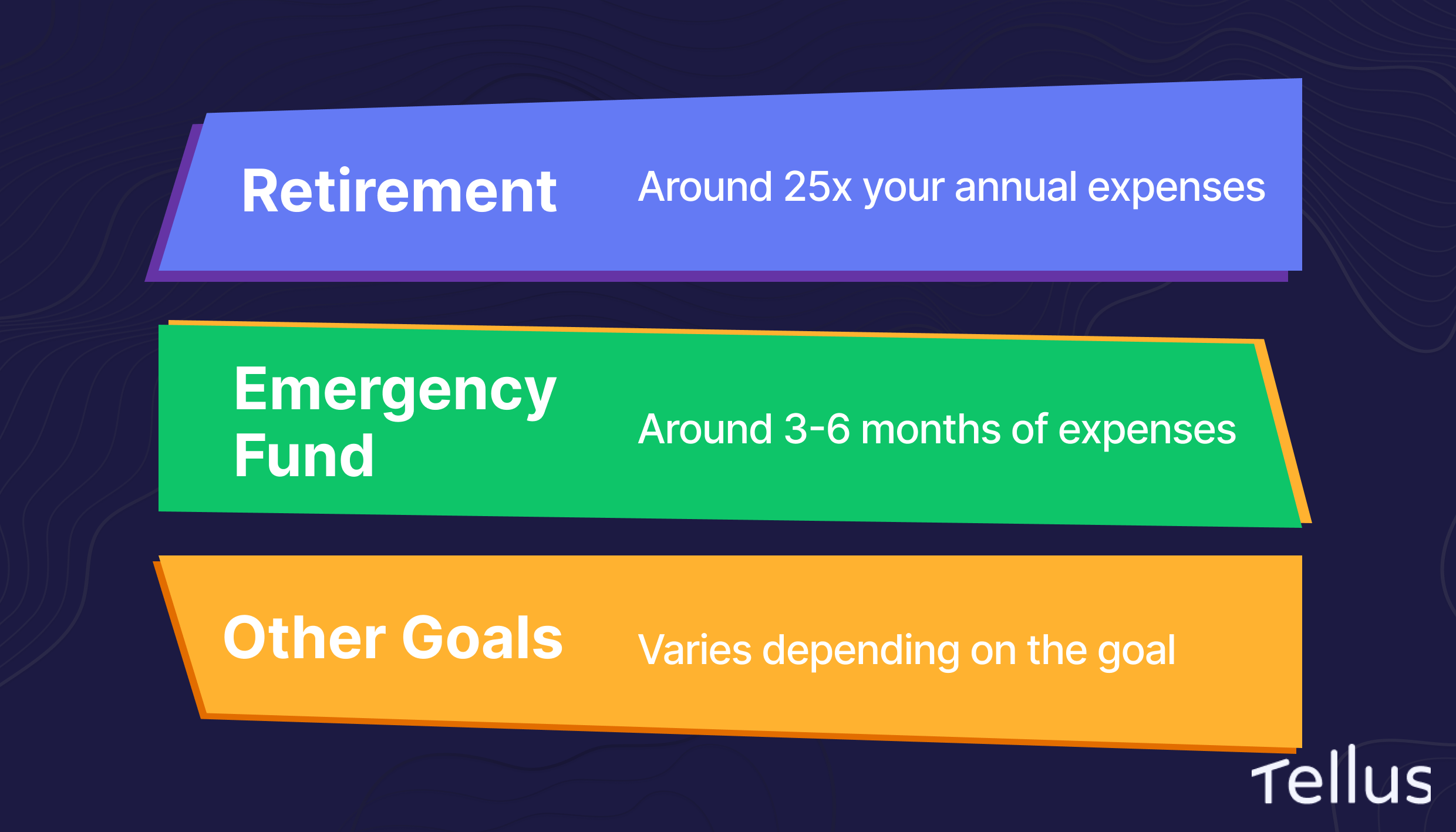

Retirement

Retirement should be a top financial priority for most people. Most households will need to save a significant amount of money in order to have a comfortable retirement.

Overall, you should aim to save around 25x your annual expenses. If you spend $40,000 per year, you’ll need around $1 million saved in retirement accounts. Keep in mind that this all depends on your sources of retirement income, whether you have a pension, and other factors.

Many people plan to rely on social security, but the average social security check is only around $1,500. That means most households will have to make up the difference with their own savings (or pensions from their workplaces), or risk having to sell their house or severely downgrade their lifestyle in retirement.

Retirement savings should be placed in dedicated retirement accounts, which offer generous tax benefits. Funds should also be invested so that they can grow. Here’s a very brief list of what you should prioritize when it comes to saving for retirement.

1. Check with your employer about their retirement plans

First, ensure you’re utilizing employer benefits — particularly if your company matches your savings (more on this later). Ask the human resources department what plans are available and how they work.

2. Open your own retirement accounts

If your employer doesn’t have a retirement plan (or the options are bad), you may wish to open your own account. You can do this at a stock broker, like Schwab or Fidelity. A popular account option is the Roth IRA.

3. Make sure you’re investing

Retirement savings should typically be invested in assets like stocks or bonds. This will allow your money to grow over time. If you’re unsure how to start, buying a simple index fund is wise. Buying an S&P 500 index fund is like buying a very small slice of the 500 largest companies in America — and it takes just a few clicks on a stock broker’s website.

Retirement planning is important. If you’re unsure how much you need or how to go about saving, it’s wise to talk to a financial advisor.

Emergency fund

Another financial priority should be saving up for an emergency fund. This is a dedicated chunk of savings for unexpected expenses and unexpected loss of income. Emergency funds should be kept in liquid savings that can be accessed at any time.

The common recommendation is to have 3 to 6 months of basic expenses saved in an emergency fund. So if you spend $3,000 per month, you should aim to save between $9,000 and $18,000 in your emergency fund.

Major purchases & renovations

Saving up for major expenses — a future wedding, a new car, etc. — is another category of savings goals. This could also include saving up for a down payment or renovations on your existing home.

The amounts needed and timelines for these goals vary significantly. It’s a good idea to sit down and map out your goals, working backward to find the monthly amount you need to save to stay on target.

Other savings goals

Finally, there are various other savings goals that you may have. You may wish to save up for an international trip or save for your child’s future education. There’s no rule-of-thumb for how much to save here — it just depends on your goals.

Whatever the goal, it’s helpful to make a plan for how to reach it. And remember that you can work toward several goals all at once — just make a plan, and split your savings toward different goals according to that plan.

At Tellus, we’ve made it easy to visualize your goals with a feature called Stacks.

How to save more money

Saving money helps you reach your financial goals and reduce financial stress. But how can you maximize the amount you are able to save?

Below, find money-saving tips to help you reach your goals faster.

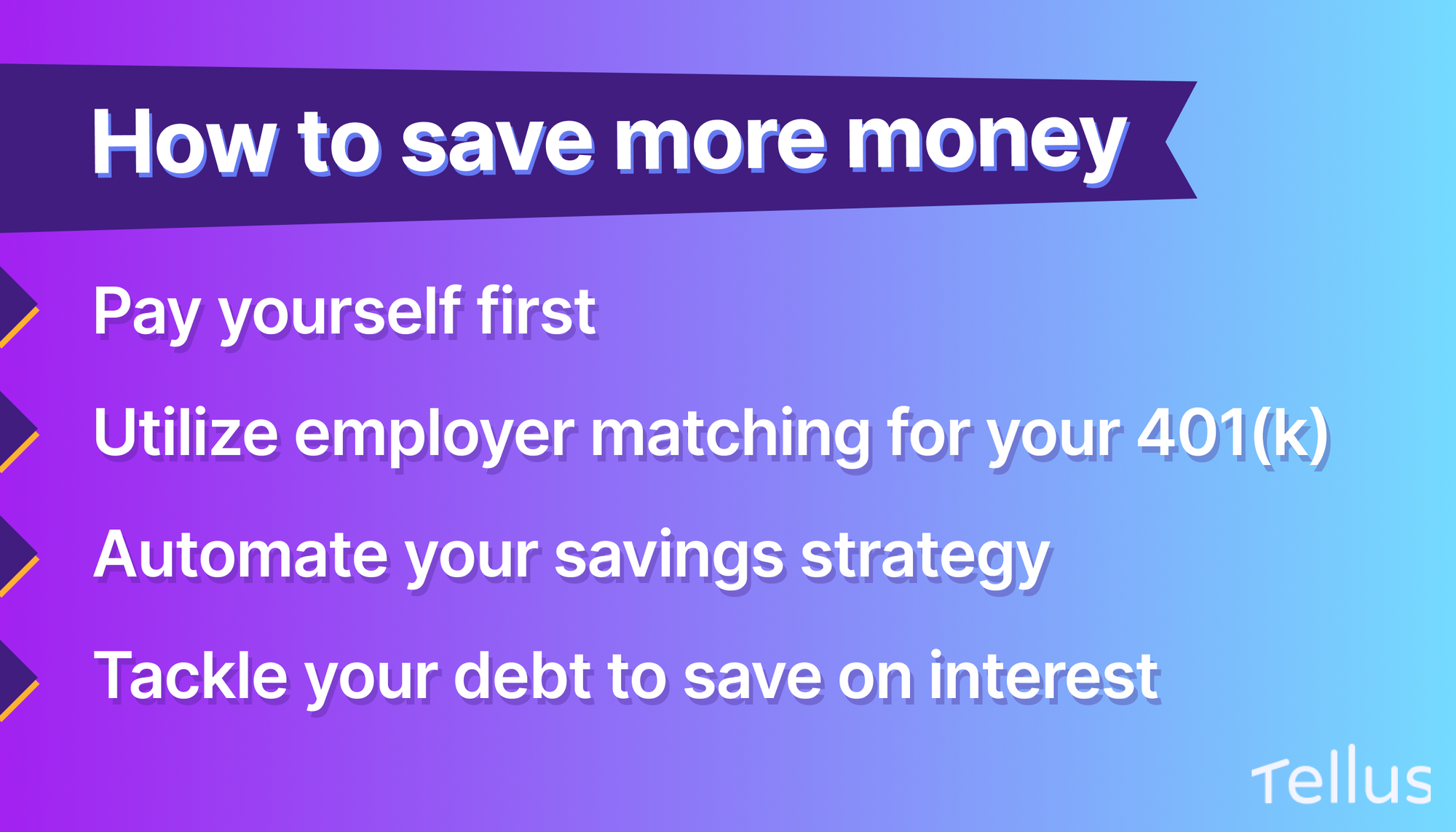

Pay yourself first

A simple yet powerful concept is to pay yourself first.

Whenever you receive a paycheck, transfer funds into savings before paying any of your bills or buying anything.

In this way, you are consistently prioritizing your own savings goals over the various expenses you have. It sounds simple, but it can make a huge difference toward staying consistent with your savings.

Take advantage of employer matching

If your employer offers a 401(k) or another retirement plan, ask if they offer “matching.”

Matching is a powerful job benefit that is available to many employees. If an employer offers 401(k) matching, this means that they will match a percentage of the amount you save toward retirement.

For example, an employer might offer a 100% match on up to 5% of your salary. If you earn $50,000 annually, your employer will match the first $2,500 you contribute to your 401(k) each year. If you save $2,500, you’ll end up with $5,000 in your account!

Matching details vary significantly, and not all employers match — but it’s 100% worth asking your workplace's HR department about your benefits.

Automate your savings

Another simple yet powerful trick is to set up automatic transfers to your savings and investment accounts.

Most banks and financial institutions allow you to set up automatic weekly or monthly transfers.

For example, you could set up automatic transfers for:

- $200 per month to your retirement account

- $100 per month to your emergency fund savings account

- $100 per month toward your general savings account

You can time these automatic transfers to go out shortly after you receive your paycheck.

Tackle your debt

Paying off high-interest debt can also help save you money.

In some cases, repaying debts should be a priority for your “savings.” You may not think of this as saving money, but it improves your finances in a similar way.

Paying off debt helps in three ways:

- It raises your net worth (which is calculated as assets minus debts)

- It saves you money on interest

- It reduces your future expenses by eliminating a monthly bill

For example, if you have $4,000 in credit card debt and can afford to save $500 per month, it may be wise to use most or all of that money on repaying the credit card debt.

Considering that the average credit card APR (Annual Percentage Rate) is 20%, that $4,000 in debt may be costing you $800 per year in interest — or roughly $67 per month.

Plus, once the debt is paid off, you’ll have more money in your budget to work with. You could choose to focus on paying off the debt, then catch up on your savings later.

On the other hand, if your only debt is a low-interest mortgage at 3.5%, saving or investing may make more financial sense instead of making extra payments.

If you have money in your budget to save, consider splitting it between savings and debt repayments. For example, you could use 10% to pay off debt and 10% to build your emergency fund.

Where should I put my savings?

Saving money is one thing, and knowing where to actually put that money is another altogether.

- A bank savings account — simple and free but pays very little interest

- A high-yield savings account — pays a bit more interest

- Savings bonds — offer decent yields, but lock your money up for a period of time

- Certificates of Deposit — offer higher yields than bank accounts, but lock your money up for a period of time

Then there are accounts that are beneficial for certain types of savings. Here are the basics:

Retirement savings should generally be kept in retirement accounts, as they offer generous tax benefits. Retirement account options include Roth IRAs, 401(k)s, and more.

College savings should often be kept in college savings plans, as they offer tax benefits. One popular option is the 529 plan.

Wrapping up

The common rule of thumb is to save 20% of your monthly income. With that said, any savings is better than none. If you’re struggling to tuck away 20% of your paycheck, don’t be discouraged — save what you can, and you’ll still make progress toward your financial goals.

{kind=link}